831 (b) Captive Articles and News

831(b) captive insurance companies are small insurance companies that qualify for a special election under the US tax code section 831(b) if they are design and formed as legitimate insurance companies that qualify for and properly make the election. Substantial US tax incentives enacted in nearly 30 years ago exist to encourage their formation where a small insurance company is needed to efficiently finance insurable risks. Due to concerns over use of 831(b) captives by tax shelter promoters, the IRS has increased its scrutiny of 831(b) captives in recent years, although stating it does not intend to chill the use of the 831(b) election by legitimate small insurance companies with primary purpose of improving risk management.

For a helpful financial projection showing the potential impact on the level of investment asset a business can accumulate to protect it from unexpected losses when owning an 831(b) captive verses not owning an 831(b) captive, click here. 831(b) captives properly designed also reduce the expense of commercial insurance and can help stabilize insurance costs.

Below are some excellent introductory 831(b) articles and information.

Click here to read an excellent 831(b) captive insurance company benefits article, most of which is inserted below.

Click here to read an March 2013 Journal of Accountancy article with good case study on benefits of a 831(b) captive integrated with estate planning.

****************************

831 B Captive Tax and Financial Planning Primer

(c) Tom Cifelli, March 23, 2012.

Introduction

The US Congress in 1986 adopted section 831(b) of the Internal Revenue Code of 1986 specifically to encourage micro captive insurance formations to strengthen US businesses, and created a significant tax incentives for doing so.

Despite this tax incentive provision being nearly 30 years old, most professional business advisers still do not understand 831(b) captives and as a result tens of thousands of small to medium sized businesses (SMBs), the backbone of job growth and innovation in the US economy, that could benefit by using 831(b) captives have not yet been introduced to them.

Follow these links to learn why 831(b) captives are increasingly popular to help businesses be more competitive and grow assets faster:

- Summary article on estate planning integration and tax leveraging benefits (be aware the IRS has stated its belief that advanced ownership structures integrated with 831(b) qualifying captives to afford asset protection and estate planning benefits may be deemed abusive on review if tax savings are the primary reason for such ownership structures);

- Captive Tax Planning Primer (again be aware if tax savings is your primary objective for forming a captive it is best if you do not do so today given the IRS's hostility towards use of captive insurance companies primarily for tax minimization, and not primarily for improving enterprise risk management and loss reserve finance).

Just as individual financial and tax planning advisers need expertise in retirement planning, all business financial and tax planning advisers need expertise in 831 B captives as they truly can help protect and strengthen SMBs and the families that own them. These benefits are not limited to US owned businesses. Many companies in other countries could benefit from creating a captive.

A privately held 831 B captive can save up to $500,000 annually in income taxes allowing that extra cash to be retained within a business family to protect and strengthen the business enterprise group.

Properly designed and managed, these protective loss reserves can accumulate outside of the business owner's estate, protecting assets and enabling small business to survive unexpected disruptions and more easily accumulate business succession reserves.

Since small to medium sized businesses are the backbone of the US economy, job growth and innovation, the underlying tax policy objectives of IRC section 831(b) are clearly in the nation's best long-term interest. Advisers need to increase expertise in 831(b) captives and better educate small to medium sized businesses on these valuable and greatly under-utilized advanced business risk planning vehicles. These tax advantaged small captive insurance companies accelerate reserve asset accumulation by closely held businesses.

Provided you design your 831 B Captive correctly to meet business purpose and economic substance tests, this special IRC code section 831(b) election allows an operating company to deduct premiums paid while allowing the related party captive insurance company to exclude the premium income from federal income tax (forever not just deferred). Most domiciles that license and regulate captives also allow the ownership to be structured so the captive's asset reserves accumulated are not in the estate of the owners of the insured related operating companies.

Importance of 831(B) Captives

Consider by contrast why so many successful business owners invest in retirement plans. The US government enacted income tax deferral provisions specifically aimed to encourage retirement savings. The US government went even farther with properly designed and operated 831B captives. This makes perfect sense verses thinking it is some tax loophole. Small to medium sized businesses (SMBs) account for the majority of job growth and innovation in the US. It is clearly in the USA's strategic interest to encourage these SMBs to create protective reserves. Doing so not only makes them more competitive, but designed correctly increases business succession financing options.

If the 831b captive builds sufficient reserves, it can expand its insurance program to greatly reduce expense of commercial market policies as well as expand employee coverage offerings (like medical stop loss) at more affordable rates.

Various Uses of 831 B Captive Asset Reserves

These tax leveraged asset reserves accumulating in your 831b captive (assuming of course policy losses are low due to effective risk safety and management practices) can be used for a variety of purposes unless you select an overly restrictive regulatory domicile for formation:

- loaned to the insured operating companies who paid the premiums (or other family businesses);

- invest in related family businesses;

- invest in real estate (unlike retirement plan assets which have restrictions against related party loans or investments);

- distributed as dividends which are historically taxed at more favorable rates;

- on wind-up capital distributions are also historically taxed at lower rates than the value of the deduction when premiums were paid; and

- for the most sophisticated entrepreneurial families, the life cycle of an 831b captive can involve it exiting the insurance business, retaining its accumulated reserves, and evolving into a family fortress entity of one type or another (unregulated or regulated depending upon the family's sophistication and advisory team vision).

Most of the restrictions that apply to retirement plan assets do not apply to excess reserves in your 831b captive. They simply are a superior business and risk management engineering tool to retirement plans for high net worth owners of successful businesses. But for the costs of creating and managing an 831 B Captive, certainly many more businesses would utilize them.

Tax Summary

Internal Revenue Code section 831(b) exempts, not merely defers, all operating income from qualifying captive insurance companies from federal income tax. This special tax benefit encourages small and mid-market sized companies to create protective risk reserve assets. As mentioned earlier, structured correctly, important asset protection and estate planning objectives are also easily achieved adding another layer of protection and expanded business succession capacity. For a general introduction to captive insurance taxation issues, click here.

The 831(b) election allows a small insurance company to receive up to $1.2 million per year in premiums, without paying any income taxes on those premiums (while the related party operating company insured deducts the premiums against ordinary income). The 831(b) election is not available to larger captives. They do however still benefit from general insurance accounting and tax advantages enabling deduction of reserves against uncertain future losses, a special accrual accounting benefit available only to licensed insurance companies.

The significant advantage of the 831(b) election is that the company is able to accumulate surplus from underwriting profits free from tax without need of use of the restrictive and complex typical insurance company reserve accounting. This 831(b) tax advantage greatly leverages a small businesses capacity to built risk reserve assets which they retain investment control over verses losing control forever of premiums paid to unrelated traditional insurers or continuing to self-insure with after-tax dollars significant enterprise risks. When integrated with estate plans, the wealth protection and accumulation benefits can be substantial.

While IRC Section 831(b) provides special income tax exemption benefits to underwriting premium revenue of $1,200,000 or less each year from federal income tax, investment income is still taxed. This special tax benefit helps place small privately held captives insuring risks of affiliated businesses on a level playing field with much larger commercial insurers who have long benefited by special accounting and tax law provisions.

If the 831(b) election is abused, the IRS could not only deny the deduction to the operating company who paid the premiums, but also tax the captive on its premium income. Substantial penalties and interest could also apply if the IRS deems the structure abusive. So care must be exercised to not be creating an 831 B Captive merely for tax savings; real business and non-tax economic purpose must be objectives of the design and operating decisions.

Current Uses of 831 B Captives

Surveys of these small to mid-market sized companies confirm nearly all are increasingly concerned about enterprise and catastrophic risks, generally uninsured prior to formation of a captive, ranging from technology risks, regulatory risks, key employee risks, key customer risks, key supplier risks, and other catastrophe risks. Once these smaller companies become familiar with captive insurance, they often expand the captive program scope to make them more competitive, improve safety programs and initiatives, and better weather hardening insurance markets.

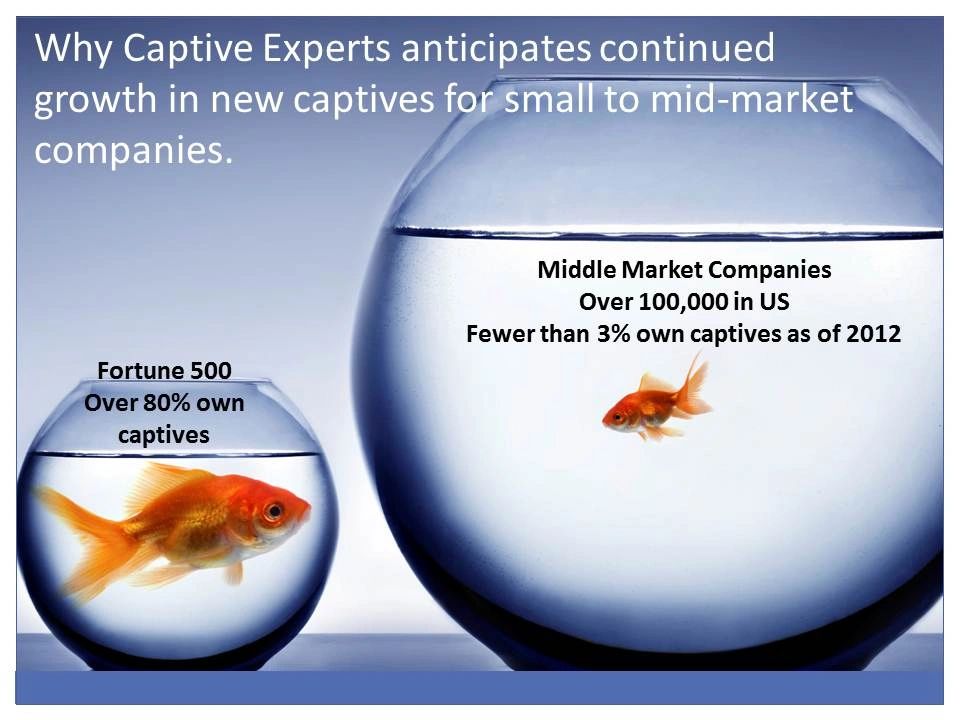

Captive formation in the US is a relatively new legal phenomenon. That is why few people know what they are. Vermont was the first state to dedicate insurance department staff to encourage captive formations in the early 90s. Now 20 years later, over 30 US states authorize captive formations. While nearly all Fortune 500 companies today have formed a captive, the special 831(b) tax election available only to small captives has created the needed incentive for smaller closely held businesses to take advantage of them to become stronger and more competitive.

Future of 831 B Captives

Internal Revenue Code section 831(b) captive insurance companies accounted for most new US taxpayer owned captive formations in 2010 and 2011. Nearly all were formed by small to mid-market closely held family businesses and some successful professionals, especially medical and high-tech professionals.

Among elite business financial advisory firms, captives are becoming increasingly popular as these advisers understand how a captive fits with many of their successful business clients, usually high net worth families.

More Observations of Interest on 831 B Captives

While many states approved new 831(b) captive applications in 2010 and 2011, Delaware and Utah experienced the highest percentage growth rates among US domiciles due to low fees and high quality service. A few offshore domiciles, with low initial capital requirements and efficient regulatory systems, continue attracting 831(b) captive insurance company business from US owners due to Internal Revenue Code section 953 elections which allow these foreign domiciled companies to be taxed as a US taxpayers, thus qualifying these foreign domiciled captives for the 831(b) election. This also allows a foreign domiciled captive to avoid the US foreign excise tax on non-admitted premiums.

US based Cell and Series LLC programs allow the greatest flexibility, easiest application process, and enable initial capital lower than foreign domiciles in some cases. As familiarity with the handful of well run Series LLC and cell programs rises, we expect wider use by smaller privately help companies across all industries to form 831b captives. The most sophisticated will pursue 3rd party risk underwriting they understand and have an existing business connection to (such as Best Buy and Verizon's captives writing product replacement and warranty coverage of their customers) in order to increase underwriting profits of the captive and turn it into a true profit center.

Costs to Form and Operate Small 831 B Captives (see detailed excerpt at the end of this page that lays out costs and estimates in detail to form and operate a 831(b) captive)

Total formation and annual operating costs can be kept as low as $25,000 including domicile expenses although well established and properly staffed firms cannot maintain high service levels and trained back-up staff without charging more than this. Going with the lowest cost service providers is not well advised in this industry as quality varies greatly. Click here to read a well written brochure on 831(B) Captives prepared by Wilmington Trust - note it shows the higher end of the costs to form and operate a 831(b) captive. We have helped initiate 831(b) captive programs for much smaller companies at far less expense while still using top shelf world leading service providers.

Risk pool fees may also apply in order for the 831 B captive to meet risk distribution requirements (of the IRS for US based insureds) in order for the captive to be considered an insurance company for US tax purposes. Well run risk pools are careful not to accept high risks. Many companies interested in forming a captive are determined unqualified due to their risk management characteristics not meeting pool underwriting requirements. See our taxation discussion for more information on risk distribution and other tax requirement issues.

The minimum required start-up capital of your captive varies greatly. Joining an existing program cell or series program requires far less start-up capital and reduced operating costs than stand alone pure captives. Most new 831(b) captive owners join existing cell or Series LLCprograms due to the lower cost of entry and operation. Most US domiciles require $250,000 minimum initial capital and surplus to form your own captive, which is an arbitrary number states seem to have adopted when copying each other's captive statutes. Some very experienced domiciles allow captive formation with as little as $25,000 in initial start-up capital and surplus. We predict at some future point, some US domiciles will follow with risk based minimums verses the current $250,000 arbitrary minimum of most of not all US domiciles.

Click here to read the full article.

***********************

Expanded Useful Information Impacting 831 B Captives Follows:

************************

Click here to read this August 2012 article on coming tax, legal and financial controversies involving 831(b) captive practices.

************************

The area of independently procured self procurement retaliatory premium taxes is perhaps the least understood and settled area and could cause a surprise expense for many of these newly formed 831b captives that elect to domicile in a state or country other than the home state of the insured companies paying the premiums.

Visit our "Captive Taxation" and "More Resources" pages for access to technical white papers and related information.

***********************

***********************

Article excerpts below. Visit other areas of this site to read full featured articles andwhite papers on hot topics.

*****************

831(b) Captives Lead New Captives Formation - Primer and Update on These Special Tax Advantaged Closely Held Small Business Insurance Companies, by Tom Cifelli, November 2011 (All Rights Reserved)

INTRODUCTION

Completing a custom feasibility study determines whether an 831b captive program works for you. In ideal situations, a business can deduct up to $1,200,000 in premiums it pays to its affiliate 831b captive, reducing the operating company income tax by over $400,000 in many cases, with the 831b captive premium income exempt from income tax. These special small captives can be set up and managed professionally for the first year for $50,000 or less in total expenses in many cases with the owner retaining control of the captive assets to invest or even make loans back the operating company. If integrated with estate plans, after tax cash is significant and enables building a stronger company creating more jobs quickly. The US government encourages use of this advanced planning technique to protect and strengthen small US businesses, the true job creators who are a core part of, the most exciting part of, the future US economy. Learn how to start taking advantage of this advanced financial and business planning opportunity now by contacting us.

MORE INFORMATION

Companies that have a good claims history, that want to cover "hidden risks" including existing policy exclusions and deductibles, and can also benefit from the special operating income tax exclusion, can use 831(b) captives:

- to retain profits being made by 3rd party insurance companies,

- to use pre-tax dollars to fund risks currently self-insured with after-tax dollars;

- to protect assets from creditors, and

- to expand retirement income and estate planning options.

The combination of insurance savings, expanded risk management, and tax benefits are compelling. Many "new wave" domiciles make forming and operating a small insurance company affordable and easy by waiving audit, actuarial report and regulatory examination requirements typical of most larger captives.

831(b) captives account for a high percentage of total new captives being formed in recent years because they offer smaller successful companies and their owners significant operating, asset protection, wealth transfer (where the domicile will allow related parties to the insured to be the owner), and other advantages. Read more on this below.

QUALIFYING FOR THE TAX BENEFITS

To qualify for the special 831(b) tax election, annual insurance premiums paid your captive (not overall business premium levels) must not exceed $1.2 million. The planning opportunities are significant and private companies with multiple owners sometimes can create multiple 831(b) captives - one for each owner.

The pre-tax cash accumulating in 831(b) captives can usually be accessed if needed by the insured operating company through loans. Ultimately when the accumulated earnings are distributed as dividends or upon wind-up of the captive, they are generally subject to lower tax rates than applied to the up front deduction for premiums paid (essentially legal tax arbitrage). While tax advantages alone should not drive the decision to create a captive (see the related articles and cautions below), the tax advantages are real, significant and an intended benefit by the U.S. government for those who properly formalize risk management.

GROWTH IN USE OF 831(B) CAPTIVES

The growth in 831(b) captives is due to captive market dynamics as the industry matures. Now that nearly 90% of the Fortune 500 companies have captive insurance company programs, captive industry experts are turning their captive education and promotion attention to mid-market and smaller privately held companies. There are tens of thousands of these smaller companies who could potentially benefit from captives, and a good percentage will have sufficiently small premium levels to consider making the 831(b) election. The total number of captives today is still relatively small, approximating 6000 globally. We discuss the history of captives extensively in another article. So the growth in 831(b) captives will continue as more mid-market companies become aware of the advantages of owning their own captive insurance risk management program.

This 831(b) election can even be made by offshore captives electing to be taxed as U.S. companies. This is why a large percentage of new 831(b) captives continue being domiciled offshore. To increase transparency, strengthen your defense in the event of a future tax treatment related inquiry, and avoid increasing concerns and risk about disparity in tax treatment by the U.S. government and states for nonadmitted offshore insurance companies, selecting a U.S. domicile for your 831(B) project does seem to have some value to offset the increased costs of operations. Then again the perception that domiciling offshore is somehow "shady" is just that, a prejudicial perception, as many offshore domiciles have more experience with captives than most onshore domiciles. And they too take their responsibilities and reputations very seriously.

PLANNING CONSIDERATIONS

Most new 831(b) captives are formed to formalize an insurance program for previously self-insured or uninsured CAT (catastrophic) and other business disruption type coverage by profitable companies who find the tax savings benefit sufficiently compelling to take their first step toward formalizing an alternative risk management program by introducing a captive insurance company. Better designed 831(b) programs integrate some aspects of traditional lines of insurance coverage to achieve wider risk management objectives beyond tax advantaged reserve build-up against potential future disruptive losses.

Many 831(b) captives are owned by beneficiaries of an operating company owner. With this structure, the increase in value of the captive will be outside the owner's estate. Some domiciles require the captive owner to be the same as the insured preventing this wealth transfer benefit.

831(B) TRENDS

More than 100 831(b)s were formed in both 2010 and 2011 on and offshore. Most of these were additions to existing Series LLC programs due to the lower capital requirements and operating costs of Series LLCs verses new pure captives. This trend appears to be continuing as more small companies discover the benefits of captive insurance programs and how affordable creating and operating a small captive insurance company is today. If the general global economy picks up, this trend should accelerate.

We certainly expect to see the creative use of Series LLC and cell structures in the future that drive down cost of participation even further and make captive insurance programs available for companies of all sizes. The benefits of captives are real and are helping make US companies more competitive and create jobs.

TAX ABUSE CONCERN

Some industry observers are worried that the growth in 831(b) captives could cause problems for the captive industry if some 831(b) consultants are too aggressive promoting 831(b) programs principally on tax advantages verses risk management objectives as are generally emphasized with non-831(b) qualifying captive progams.

While the IRS may discover and correct some abusive applications of 831(b) elections, for the most part 831(b) captives serve a very legitimate and useful business planning function only recently being discovered by many businesses and professionals. Leaders in the captive industry, both regulators and captive managers, are developing useful guidelines to help prevent abusive use of small 831(b) captives. At some point additional IRS rulings should be anticipated establishing additional safe harbors for cell and series captive applications since the issues of concern to the IRS are in many respects different from that of the insurance regulators. For information about the cost of our Independent Review service for existing captive programs to help prepare them for IRS review, pleasecontact us.

While the US federal income tax advantages of qualifying as a small insurance company may be unique among for profit business corporations, this does not make use of these special provisions designed to encourage formal risk management and reserve pool funding for uncertain risk abusive in any way. There are many business development and job growth oriented tax benefits throughout the code. Suggesting the use of special tax advantaged provisions is abusive is simply being unreasonably controversial and misinformed.

Tax advantages often tip the decision making scales and many tax reform acts are designed specifically to stimulate investment including most of the 1981 Economic Recovery Tax Act enacted by President Reagan to encourage investment in commercial real estate during that recession. 831(b) is no different. It was enacted to encourage creation of small insurance companies and formalize self-insurance risk management programs and build loss reserve capital to strengthen small businesses. Many 831(b) programs are designed to cover risks the commercial insurance market does not even offer insurance coverage for.

Some observers seem worried about the growing use of tax benefits afforded by making an I.R.C. section 831(b) election. The US tax code is full of special incentives intending to impact well informed and sophisticated taxpayer behavior. In a recent conversation with an attorney with the IRS, he helped put things in perspective by commenting the decisions made by one large financial institution on loan write-downs or any other large business with troubled assets on its balance sheet could by itself impact Treasury revenue more than all the 831(b)s in the world combined. When enough small businesses have taken advantage of 831(b) and the U.S. government no longer feels it necessary to incentive more competent risk management practices by small business, or when legislators revoke further use in their quest to balance the budget, or when tax code reform eliminates our obsolete income tax system or enacts a flat tax system taking away some of the 831(b) rate differential advantages, then the 831(b) strategy will go away. In the meantime it is arguably irresponsible for successful small businesses not to consider taking advantage of 831(b) captives.

PICK THE RIGHT ADVISERS AND MANAGER

Selecting competent advisers and service providers is critical to all successful captive programs, any sophisticated business development initiative for that matter, and this is especially true of 831(b) programs. In order not to run afoul of tax regulation trouble, it is important that your 831(b) captive program be well documented, maintain timely books and records, write legitimate lines of coverage, and price the coverage fairly. For many US based owners, domiciling onshore with a US state approving the captive as an insurance company could be worth the extra cost of operating the captive onshore. The cost to form and operate a US domiciled captive continues declining with increased competition among the now more than 30 states with captive statutes.

Some states do not have premium taxes and even wave the annual audit requirement for small captives. Selecting the best domicile is not an exact science. Finding one that is receptive to your business plan without meaningfully more expensive or difficult ongoing compliance requirements are central considerations. Domiciles have a natural life cycle as well and in time most become more formalized in their regulatory requirements. For US domiciles the NAIC accreditation standards are forcing standardization and preventing many states from being more business friendly to smaller captives.

***********************

See Captive Taxation for more specific information. Forming 831(b) captives today is not expensive. The combination of insurance savings, expanded risk management, and tax benefits are compelling. 831(b) alternatives are available that in many cases are superior and more efficient for companies both too large to qualify for the 831(b) benefits and companies too small to justify a dedicated captive.

Below are other timely articles:

**********************

Section 831(b) Captives and the IRS - Underwriting and Audit Roulette, by James Landis, December 12, 2011

[Excerpt] In this timely article Mr. Landis points out the importance of setting premium levels reasonably to run afould of IRS adjustments later if your 831b captive is reviewed. He points out all too often 831(b0 promoters are not using independent underwiters or actuaries and premium levels are being set at other than "reasonable and necessary" levels for tax deductibility of any expense by a business. He also correctly points out the domicile regulators approving these 831(b) captives are not looking for this abuse as they are primarily focused on liquidity and reserve adequacy. Click here to read the full article.

**********************

Captives Could Lose Out on 'Insurance Company' Status Under IRS Rulings,by Michael Byrne, Kristan Rizzolo and Bruce Wright, published in Captive Review, July 2011.

[Excerpt] 831 (b) is a special and attractive US tax election for small captives that eliminates all income tax on operating income and taxes only investment income. Attorneys Bryne, Rizzolo and Wright confirm the IRS continues to challenge the insurance company status of smaller captives where the risk distribution elements are weakly designed. In this article they discuss recent private letter rulings where the service denied requests for 831 (b) treatment after concluding the risks were too concentrated in two related insureds. Earlier IRS rulings discussed in our Captive Taxation area explain existing safe harbors that if followed should assure insurance company tax status for your captive.

***********************

The Growth in 831 (b) Captives by Middle Market Companies Leads New Captive Formations , by CaptiveExperts.com Research Staff, June 2011

831(b) captives are very popular. 831(b) is a special insurance company election allowed under the US Internal Revenue Code. It essentially makes 831(b) qualifying captives exempt from income tax except its earnings on investment. Some captive promoters may be marketing 831(b) captives as income and estate planning tax shelters. If you form your 831 (b) in the most advantageous domiciles, there are other benefits including but not limited to exemptions from interim reporting, exemptions from annual actuarial reviews, exemptions from audits and other otherwise expensive administrative compliance rules most captives are subject to.

Caution is advised since to qualify for the 831(b) election, the captive must meet other requirements to be a valid insurance company. The election is invalid if these other requirements are not carefully met.

When properly used, the 831(b) election allows deduction of up to $1.2 million annually in insurance premiums paid by a business to its related captive while excluding that premium from captive income taxation altogether. 831(b) captives are taxed only on investment income, not operating income from its insurance business. 831 (b) captives have been the majority of US captives formed in recent years. They are almost always formed by private business owners and often used in connection with estate planning.

Some well known captive industry attorneys like Jay Adkisson caution against abusing the 831(b) small captive election. "The concept is simple: if the captive is owned by the owner's children (or a trust for those children) then the increase in value of the captive will be outside the owner's estate or gift taxes. While this wealth transfer benefit can apply to all captives, it is most often seen in the 831(b) context," states Mr. Adkinsson. Mr. Adkinsson cautions, "...it must be remembered that this is icing on the cake but not the cake itself, and not a valid justification for the captive ... first and foremost, 831(b) companies must be insurance tools to solve insurance problems, and not tax shelters disguised as insurance tools ... As with all captives, the tax tail should not wag the insurance dog." Mr. Adkisson sums up the issue as follows: "The exemption under 831(b) is not an exemption from risk shifting, risk distribution or the numerous other things that make a bona fide insurance company that is engaged in the bona fide business of insurance."

Reference Sources:

1/"Electing for Change - With the growth in middle market captive clients, will those considering the 831 (b) election meet the risk shifting and risk distribution requirements?," by Jay Adkisson, Captive Review, March 2011.

2/ I.R.C. Code Section 831(a) and 831(b)

3/ Wikipedia of Accounting for Captives, Saslow, Lufkin & Buggy, LLP, June 2011

********************

Electing for Change - With the growth in middle market captive clients, will those considering the 831 (b) election meet the risk shifting and risk distribution requirements?, by Jay Adkisson, originally published in Captive Review, March 2011.

[Excerpt] In this article, attorney Jay Adkisson cautions against abusing the 831(b) small captive election. It appears some captive promoters are marketing 831(b) captives as tax shelters, since when properly used, they allow deduction of up to $1.2 million in insurance premiums paid by a business to its related captive but excludes the premium from income taxation altogether. 831(b) captives are taxed only on investment income, not operating income from the insurance business. New 831 (b) captives have been the majority of new US captives formed in recent years. The are almost always formed by private business owners and often used in connection with estate planning. "The concept is simple: if the captive is owned by the owner's children (or a trust for those children) then the increase in value of the captive will be outside the owner's estate or gift taxes. While this wealth transfer benefit can apply to all captives, it is most often seen in the 831(b) context," states Mr. Adkinsson. Mr. Adkinsson cautions, "...it must be remembered that this is icing on the cake but not the cake itself, and not a valid justification for the captive ... first and foremost, 831(b) companies must be insurance tools to solve insurance problems, and not tax shelters disguised as insurance tools ... As with all captives, the tax tail should not wag the insurance dog." Mr. Adkisson sums up the issue as follws: "The exemption under 831(b) is not an exemption from risk shifting, risk distribution or the numerous other things that make a bona fide insurance company that is engaged in the bona fide business of insurance."

**************************

More on 831(b) captive insurance company formation costs and operating expenses:

The professional fees for leading captive insurance industry service providers with errors & omissions insurance, depth of cross-trained team, and requisite experience with regulators and taxing authorities to prevent surprises generally run $60,000 the formation year, and $40,000 to $45,000 each calendar year thereafter for small captive applications. This often includes most expenses except audits, pool fees, premium taxes and examination fees which may or may not be applicable depending on your facts and circumstances and choice of domicile. The least you should expect to invest for even the simplest captive application over its first 3 years is $100,000 "all-in" as explained in more detail by clicking here.

Having said that, the following estimates are the absolute minimum costs being quoted today by some service providers to form even the smallest micro-captive. Invariably you will be sacrificing some quality and assuming increased risks of surprises if you achieve these fee and cost levels (by contacting us you will get top shelf services at the best possible prices):

- Minimum start-up captive capital contribution to obtain approval of an application - Offshore - $10,000 (for single owner pure captives, increasing to $25k and $50k quickly depending on structure of the captive and proposed premium levels);

- Onshore - $100,000 to $250,000 (some cell and series programs allow less);

- Notwithstanding the above statement, minimum start-up capital should always be at least 10% of the planned premium level, and be at least $100,000 if you can afford it whether forming on or offshore;

- Capital and surplus to premium ratio should strive to be 3:1 initially or within the first 2 to 3 years of operation ($3 premium for $1 capital and surplus) - earnings should be retained, and distributions limited, until this is achieved;

- Feasibility and formation expenses - $25,000 for quality providers minimum; some may do it for less but rest assured you are not getting the type of underwiting, actuarial and tax analysis, team brainstorming, and documentation you will need;

- Domicile entity formation, application and licensing fees - $2,100 to $6,000;

- Domicile annual renewal fees: $1800 to $5250 (plus premium taxes in most);

- Management fees: captives need independent 3rd party management - good managers cost at least $18,000 annually for rather mall simple captives;

- Actuary: Actuaries generally cost at least $5,000 for simple captives and usually more although they may work for lower prices for larger managers bringing them dozens of new clients;

- Auditors: Any auditor who actually does the work will want $5000 or more annually even for minimal transaction activity although again some may work for less in exchange for large volumes of referrals;

- Learn about the costs to form and manage a captive by clicking here;

- In exchange for this investment, if you select qualified service providers, you will get tax advantaged loss reserve accumulations that are protected from creditors and out of your estate while retaining investment control. In fact millions more in loss reserve assets you would not have otherwise had but for owning your own captive insurance company (assuming of course you implement effective loss control and do not experience any devastating enterprise risk event which would have cost you more without a captive).

For more current information visit www.uscaptive.com and read articles published thereon.